Property Investment Guide for NRIs to Invest in Indian Real Estate

By Kolte-Patil Team | Last Updated: May 11, 2026

Key Takeaway

Considering NRI property investment in India? Here is your complete guide to investing in Indian real estate as an NRI.

Considering NRI property investment in India? Here is your complete guide to investing in Indian real estate as an NRI. Non-resident Indians (NRIs) are playing a pivotal role in the growth of India’s real estate sector. NRI investment in Indian real estate totaled US$2.3 billion in 2017, according to data from global property consultancy JLL. This significantly increased from US$1.1 billion in 2016 to US$0.6 billion in 2015.

There are several reasons for NRI investment in Indian real estate, including the desire to have a place to call home when they return to India.

Another factor is the potential for high rental yields and capital appreciation. Many NRIs are now second-generation immigrants who want to invest in their native country.

If you’re an NRI considering investing in Indian real estate, you should know a few things before making any decisions.

What Type of NRI Property Investment Is Allowed?

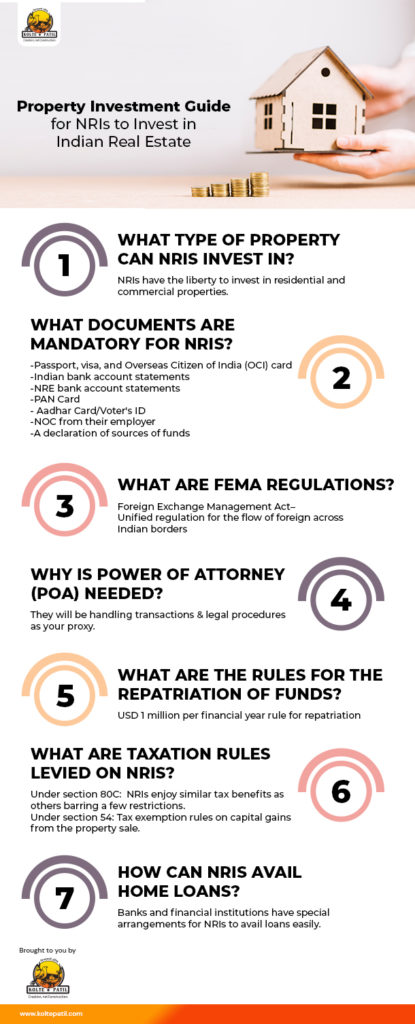

For NRI investment options, you can invest in any property in India, including residential and commercial. This also includes retail, data centers, warehouses, or any property for business.

The only restriction for NRIs is that they cannot invest in agricultural land or farms unless such property is a gift or inherited.

Documents Mandatory for NRI Property Investment

To purchase property in India, NRIs are required to submit the following documents:

-A copy of passport, visa, and Overseas Citizen of India (OCI) card

-A copy of Indian bank account statements for the past 6 months

-A copy of NRE bank account statements for the past 6 months

-A copy of the PAN Card

-A copy of the Aadhar Card/Voter’s ID

-An NOC from their employer (if employed abroad)

-A declaration of sources of funds

What are FEMA regulations & how does it benefit NRIs?

FEMA, or the Foreign Exchange Management Act, is a set of regulations that govern all aspects of foreign exchange in India. This includes investment in real estate.

FEMA was created in 1999 to replace the previous Foreign Exchange Regulation Act (FERA). FERA was seen as too restrictive and had a negative impact on foreign investment in India.

FEMA is more liberal and encourages foreign investment. Under upgraded FEMA schemes, NRIs can freely invest with regulated transactions governed by a single body. Even POIs or persons of Indian origin can invest in Indian real estate with new regulations. These millennials investing in real estate will yield the Indian market to experience projectile progress.

Why is Power Of Attorney (POA) significant?

A power of attorney is a legal document that gives someone else the authority to act on your behalf. This is the best way to invest in India for NRIs and can be used for various purposes, including financial matters.

Your POA could be a family member, friend, or professional such as a lawyer or accountant.

The POA should specify the person’s powers and how they can use them. It’s essential to ensure that the person you’re giving the POA is trustworthy and competent, as they will handle your finances.

Once you have given someone a POA, you can revoke it at any time by simply informing the person in writing that you are doing so.

What are the rules for the Repatriation of funds?

When NRIs want to repatriate their funds from India, they must first convert their Indian currency into foreign currency. This can be done through many channels, such as banks, money changers, or online currency converters. The converted funds can be transferred to the NRI’s account through wire transfer or other means.

- An NRI can only repatriate up to $1 million per financial year.

- One major rule under FEMA guidelines is that the sale proceeds are non-repatriable outside India without the RBI’s approval.

- If you have inherited the property, you can enjoy repatriation of up to $1 million per financial year.

What are Taxation rules levied on NRIs?

When investing in Indian real estate, there are a few critical taxation rules that NRIs need to be aware of.

- Any income earned from renting out property in India is subject to tax. This includes both the rental income itself as well as any associated expenses such as repairs and maintenance.

- Any capital gains made from a property sale are also subject to tax. Capital gains tax is applicable on the difference between the sale price and purchase price, typically around 20%.

- NRIs are subjected to similar taxation rules as levied on Indian residents under section 80C.

- Under section 54: NRIs should invest with the capital gains in a property 1 year before or 2 years after the sale.

It’s important to note that NRIs are only eligible for certain tax deductions and exemptions when investing in Indian real estate. So be sure to consult a professional before making any significant investment decisions.

How Can NRIs Avail Home Loans for Property Investment?

NRIs are subject to different rules and regulations when it comes to investing in property in India. There are a few things to consider for the home-buying process. Here’s what you need to know about NRI investment in Indian real estate:

- NRIs can apply for home loans directly from banks and housing financial institutions registered with the National Housing Bank.

- All transactions must be done in Indian currency only.

- A loan cannot be directly credited to an NRI’s account. The loan is disbursed to the developer’s bank account.

- They can repay their loan using their funds from NRO (Non-Residential Ordinary) /NRE (Non-Resident External) accounts or FCNR (Fixed Deposit Foreign Currency account) deposits.

A BENEFICIAL PROPERTY INVESTMENT GUIDE FOR NRIs

If you are an NRI seeking a lucrative investment in India, then a property in Pune, Mumbai, and Bengaluru has experienced substantial appreciation in recent years with projected high ROI on real estate.

Kolte-Patil Developers are the major players in Pune, with significant projects across the city. If you want to buy a property in Pune, you can choose from an array of projects with a variety of price-range, specifications, location advantages, investment benefits, and more.

Explore premium Kolte-Patil projects in Pune ideal for NRI property investment. Verify RERA registration on the MahaRERA portal.

Indian real estate remains one of the most emotionally resonant and financially attractive asset classes for NRIs, combining portfolio diversification with a lasting connection to home. With a favourable regulatory framework under RERA, clearer digital processes, and continued urbanisation across major cities, the environment for NRI investment is significantly more transparent than it was a decade ago. The key is to approach every decision with the same discipline you would apply to any serious cross-border investment.

Start by clearly defining the purpose of the purchase, whether it is long-term wealth creation, rental income, a future retirement home, or a lifestyle upgrade for visiting family. This clarity influences every downstream choice, including city, micro-market, project type, configuration, and even whether you prioritise ready-to-move-in or under-construction inventory. NRIs focused on steady rental yields typically gravitate towards well-connected metro locations, while those looking for appreciation often explore emerging corridors with strong infrastructure catalysts.

Compliance and paperwork deserve particular attention when investing from abroad. Ensure that the property is RERA-registered, that the developer has a track record of on-time delivery, and that legal due diligence, including title search and encumbrance checks, is carried out by a qualified Indian property lawyer. A carefully drafted Power of Attorney in favour of a trusted representative can simplify registration, documentation, and subsequent management if you are unable to travel for every step of the process.

Finally, build a long-term plan around financing, taxation, and repatriation. Explore home loan options from banks that specialise in NRI financing, route payments through NRE, NRO, or FCNR accounts to maintain a clean trail, and consult a tax advisor on TDS, capital gains, and DTAA benefits between India and your country of residence. Combined with prudent project selection and professional property management, this structured approach can make Indian real estate a durable, rewarding part of your global investment portfolio.

Frequently Asked Questions

What Type of NRI Property Investment Is Allowed?

For NRI investment options, you can invest in any property in India, including residential and commercial. This also includes retail, data centers, warehouses, or any property for business. The only restriction for NRIs is that they cannot invest in agricultural land or farms unless such property is a gift or inherited.

What is Documents Mandatory for NRI Property Investment?

To purchase property in India, NRIs are required to submit the following documents: -A copy of passport, visa, and Overseas Citizen of India (OCI) card

What are FEMA regulations & how does it benefit NRIs?

FEMA, or the Foreign Exchange Management Act, is a set of regulations that govern all aspects of foreign exchange in India. This includes investment in real estate. FEMA was created in 1999 to replace the previous Foreign Exchange Regulation Act (FERA). FERA was seen as too restrictive and had a negative impact on foreign investment in India.

Why is Power Of Attorney (POA) significant?

A power of attorney is a legal document that gives someone else the authority to act on your behalf. This is the best way to invest in India for NRIs and can be used for various purposes, including financial matters. Your POA could be a family member, friend, or professional such as a lawyer or accountant.

What are the rules for the Repatriation of funds?

When NRIs want to repatriate their funds from India, they must first convert their Indian currency into foreign currency. This can be done through many channels, such as banks, money changers, or online currency converters. The converted funds can be transferred to the NRI’s account through wire transfer or other means.

What are Taxation rules levied on NRIs?

When investing in Indian real estate, there are a few critical taxation rules that NRIs need to be aware of. It’s important to note that NRIs are only eligible for certain tax deductions and exemptions when investing in Indian real estate. So be sure to consult a professional before making any significant investment decisions.

How Can NRIs Avail Home Loans for Property Investment?

NRIs are subject to different rules and regulations when it comes to investing in property in India. There are a few things to consider for the home-buying process. Here’s what you need to know about NRI investment in Indian real estate:

What is A BENEFICIAL PROPERTY INVESTMENT GUIDE FOR NRIs?

If you are an NRI seeking a lucrative investment in India, then a property in Pune, Mumbai, and Bengaluru has experienced substantial appreciation in recent years with projected high ROI on real estate. Kolte-Patil Developers are the major players in Pune, with significant projects across the city. If you want to buy a property in Pune, you can choose from an array of projects with a variety of price-range, specifications, location advantages, investment benefits, and more.